Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

May Flowers? The Headline vs. The Underlying Data

Last month I told you I’d be watching new pendings closely. They didn’t bounce back. But the listings I expected to keep piling up didn’t show either, so the “rebalancing” I floated for June didn’t arrive the way I thought it would. Instead, May handed us something more interesting. Here’s the link to the data:

May Flowers?

The saying goes that April showers bring May flowers. This May, the prices bloomed, but the volume wilted. The headline numbers are still sunny. The activity underneath them has gone quiet in a way we haven’t seen in a while, and that quiet is the real story this month.

Single Family Homes (Page 1)

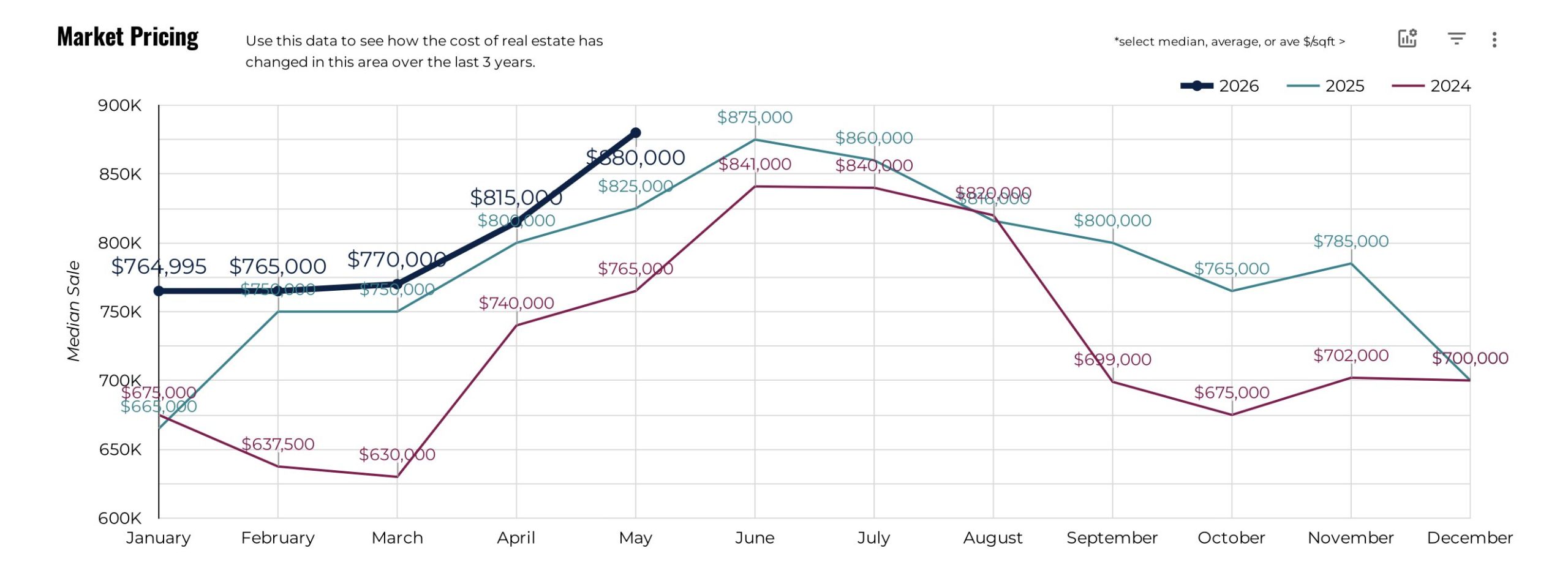

On the surface, May kept the streak alive. Median sale price rose to $880,000, up 6.7% year-over-year. Average sale came in at $1.3M (up 5.0%). Price per square foot reached $440 (up 3.9%). If you only read those three numbers, nothing has changed.

But look at the volume behind them (Page 1):

- Total volume came in at $631.7 million, down 7.5% from last May.

- Closed sales fell to 477, a 12.0% drop year-over-year.

In other words, fewer homes are trading hands, even as the ones that do sell for more. Now go one layer deeper (Pages 2 and 3):

- Median days on market rose from 10 last May to 16 this May. Average DOM climbed from 28 to 35.

- Buyers actually paid more over asking this time: 4.62%, up from 3.80% a year ago.

- New listings (supply) were down 4.9% year-over-year.

- New pendings (demand) were down 14.5%.

That last pair is the one I want you to sit with. Last month, listings were rising and I thought supply was finally arriving. This month, supply reversed and pulled back, and demand fell even faster. Months of supply actually tightened to 2.23 (anything under 3 still favors sellers). So we don’t have a glut of homes sitting around. We have fewer homes coming to market, fewer buyers going under contract, and a smaller number of strong, well-positioned sales holding the price line (and even drawing buyer competition) at the top.

Condos (Page 4)

Condos rhyme with the single family story, but the bidding heat is gone. Median sale was $430,000 (up 7.8%), average sale was $525k (up 4.1%), and price per square foot hit $356 (up 1.8%). Strong on paper.

Underneath (Pages 5 and 6):

- Median DOM doubled, from 11 to 22 days. Average DOM rose from 28 to 37.

- % over asking collapsed from 1.94% to 0.97%, essentially asking-price territory.

- New listings were down 5.2%, while new pendings dropped 17.7%.

- Closed sales fell to 188 (down 16.1%) and total volume slid to $98.9 million (down 12.7%).

The condo segment is still pricing strongly off prior months, but buyers have stopped competing. They’re showing up at the table and, more often than not, paying the number on the sign.

What’s Going On?

A standoff. Sellers aren’t listing, many are holding low interest rate loans, watching headlines, or simply unconvinced it’s their moment. Buyers are pulling back even harder, whether from rate fatigue, thin inventory, or plain selectivity. When both sides step back at once, you don’t get a price crash. You get a freeze: fewer listings, fewer contracts, fewer closings, and prices that hold (or rise) because the trickle of supply still can’t quite meet what demand remains, especially for single family homes.

This is not a market crash. It’s a market that got quiet. We’ve moved from “everything well-priced sells fast” to “very little is changing hands at all, but what does is still getting a strong number.”

What Does it Mean?

Buyers: The breathing room I mentioned in April has partly closed, at least on the single family side. There’s less to choose from than a month ago, and the good single family homes are drawing competition again (over-ask premiums went up, not down). Condos are the exception, that segment is genuinely negotiable right now, often at or below asking. If you’re a condo buyer, this is your moment. If you’re after a single family home, be ready to move decisively when the right one lists, because it won’t sit.

Sellers: The scarcity is quietly working in your favor. New listings are down, which means less competition than you’d expect, and single family buyers are still paying over asking for the right home. That doesn’t mean you can skip preparation. The market is rewarding well-priced, well-prepped homes and ignoring everything else, exactly like the frenzy years, just at a lower volume. Condo sellers: price at market and don’t count on an over-ask premium, it isn’t there this month.

Looking Ahead

The swing factor is still new pendings, and they’ve now declined two months running. If listings stay scarce and pendings keep sliding, we’re looking at a genuinely low-transaction market for the back half of the year: high prices, thin volume, long stretches between deals. If summer thaws either side loose, more sellers listing or more buyers committing, the picture opens back up quickly. I’ll be watching which one moves first.

As always, reach out with any questions, I’m happy to chat!